Introduction

Large Language Models (LLMs) have rapidly become the cornerstone of today’s AI revolution, reshaping how individuals, enterprises, and entire industries interact with technology. From consumer-facing chatbots to enterprise-grade analytical tools, LLMs are driving a new wave of productivity, creativity, and automation.

Yet, behind the excitement lies a highly dynamic and competitive market landscape. Global leaders such as OpenAI, Anthropic, and Google are not only racing to build the most capable models but are also shaping business models, regulatory debates, and investment flows that will define the next decade of AI adoption.

To better understand this evolving ecosystem, we leveraged Powerdrill Bloom to conduct a comprehensive analysis of the global LLM market. This research explores current market dominance, revenue strategies, growth trajectories, and the future outlook for large language models. The findings provide actionable insights for businesses, investors, and technology leaders seeking to navigate one of the fastest-growing and most transformative markets of our time.

How to Get Started with Powerdrill Bloom

Sign in to Powerdrill Bloom.

Click Start Blooming, then choose Start from a topic, enter your topic, and click Start Research.

For example: Analyze the current global market landscape of the most popular large language models and their future trends.

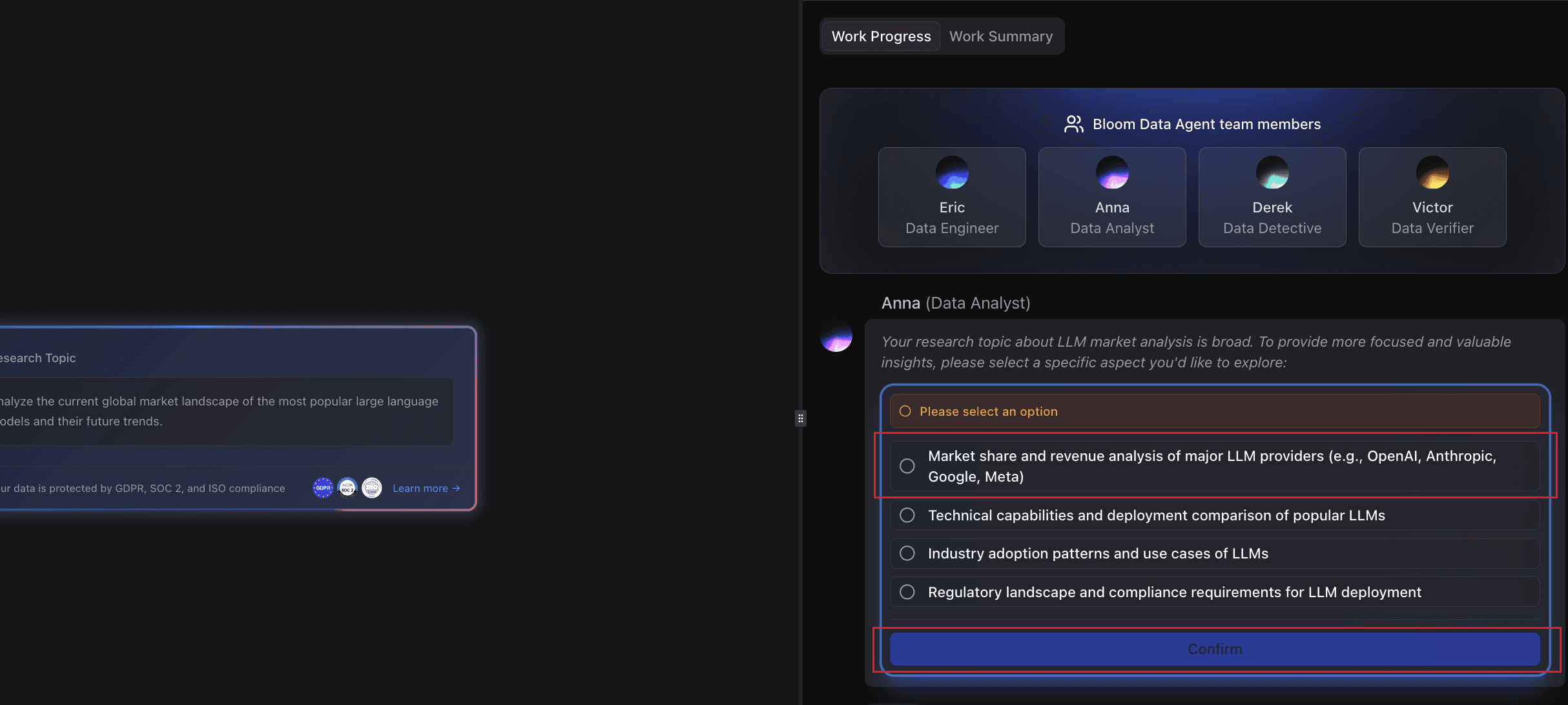

Choose the option you're interested in, and click Confirm.

For example: Market share and revenue analysis of major LLM providers (e.g., OpenAI, Anthropic, Google, Meta)

Let's see the results Powerdrill Bloom presents.

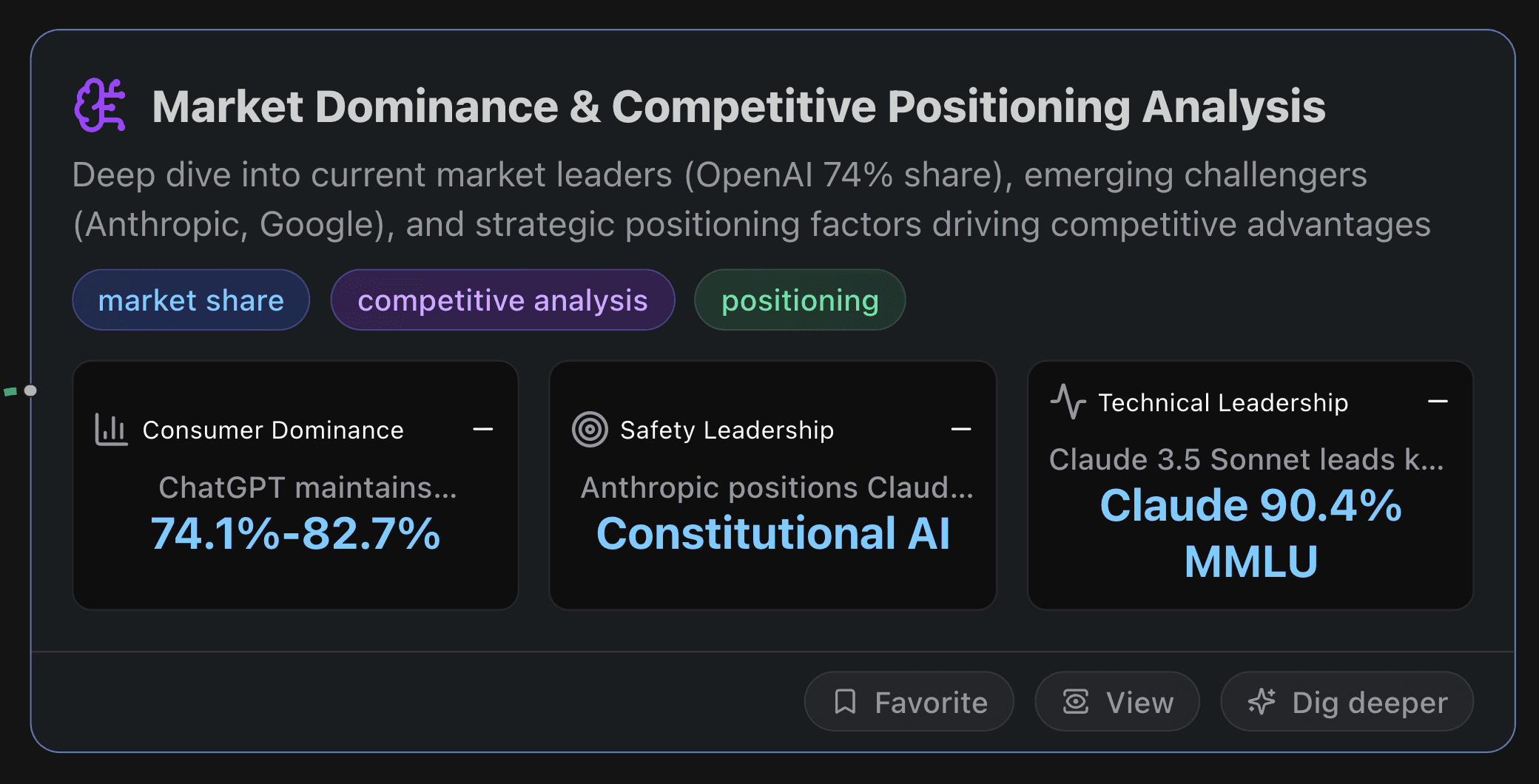

Market Dominance & Competitive Positioning Analysis

This node dives deep into current market leaders (OpenAI 74% share), emerging challengers (Anthropic, Google), and strategic positioning factors driving competitive advantages.

Key Metrics

Consumer Dominance

ChatGPT maintains overwhelming consumer market leadership with consistent 74% share based on chatbot usage metrics, reaching up to 82.7% when measured by website traffic. This dominance stems from first-mover advantage, extensive marketing, and Microsoft partnership providing distribution through multiple channels.

Safety Leadership

Anthropic positions Claude through 'Constitutional AI' methodology and transparency-first narrative, contrasting with OpenAI's criticized secretive approach. This safety-first positioning captures enterprise customers in regulated industries requiring compliance and trust, particularly in healthcare and finance sectors.

Technical Leadership

Claude 3.5 Sonnet leads key benchmarks with 90.4% MMLU score versus GPT-4o's 88.0%, establishing technical performance edge in structured reasoning tasks. This benchmark leadership supports Anthropic's positioning for complex enterprise analytical workloads requiring high accuracy.

Actionable Insights

Enterprise-First Positioning Strategy

Given Claude's rapid enterprise market share growth from 18% to 29% while OpenAI dropped from 50%, companies should prioritize enterprise-specific features like enhanced security, compliance certifications, and transparent AI governance. Focus on regulated industries (healthcare, finance) where safety-first messaging creates competitive differentiation and commands premium pricing.

Multimodal Capability Investment

OpenAI's native multimodal advantage with GPT-4o's real-time processing maintains consumer dominance at 74% market share. Competitors should accelerate multimodal development investments, particularly in video and voice capabilities, to challenge OpenAI's technical moat and capture share in creative and interactive use cases where multimodal experiences drive user engagement.

Ecosystem Integration Strategy

Google Gemini's 37% US market share in document-centric tasks through Workspace integration demonstrates ecosystem lock-in effectiveness. Companies should pursue strategic partnerships with major software platforms (Microsoft, Salesforce, Adobe) to embed AI capabilities directly into user workflows, creating switching costs and reducing competitive vulnerability from pure-play AI providers.

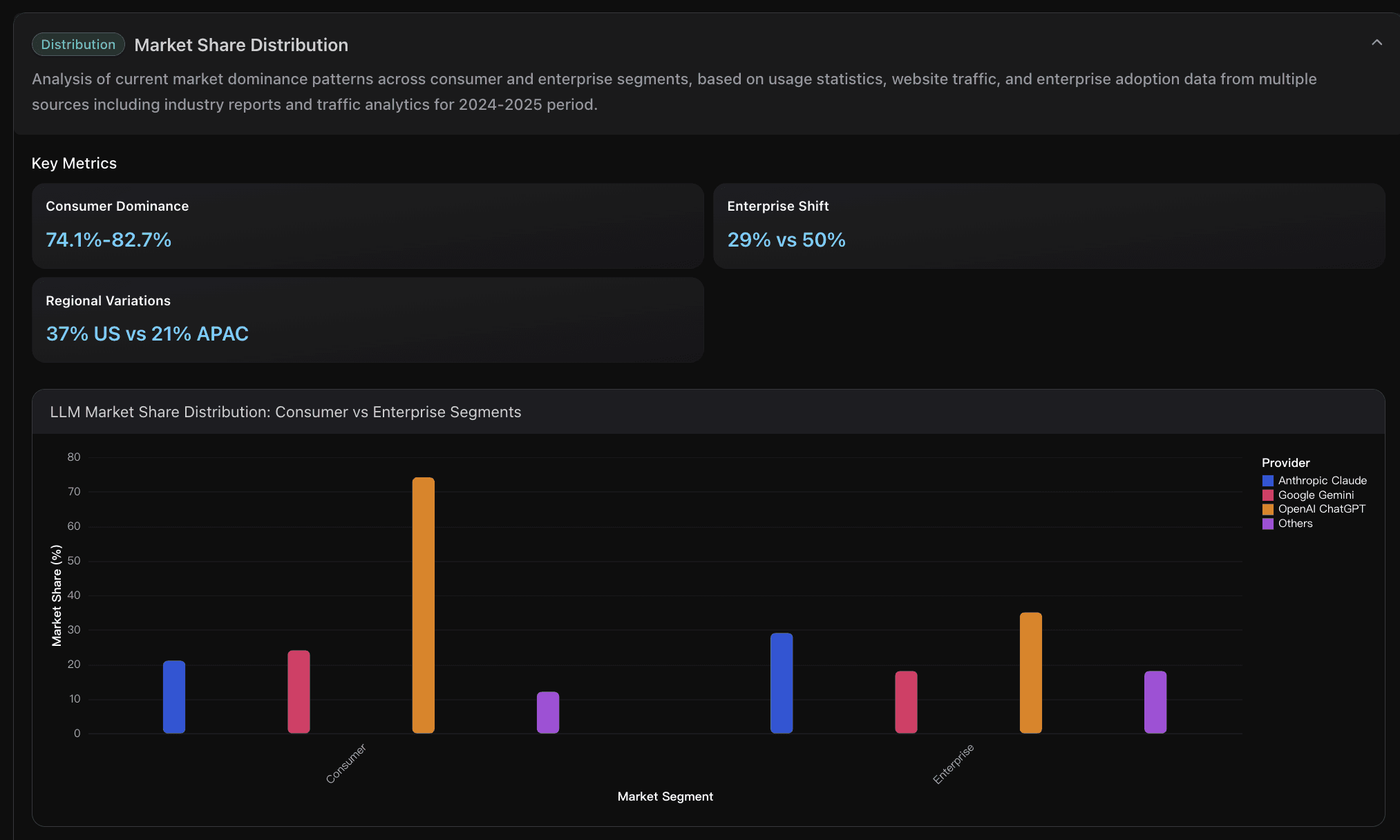

Data Visualization

Below is a data visualization example:

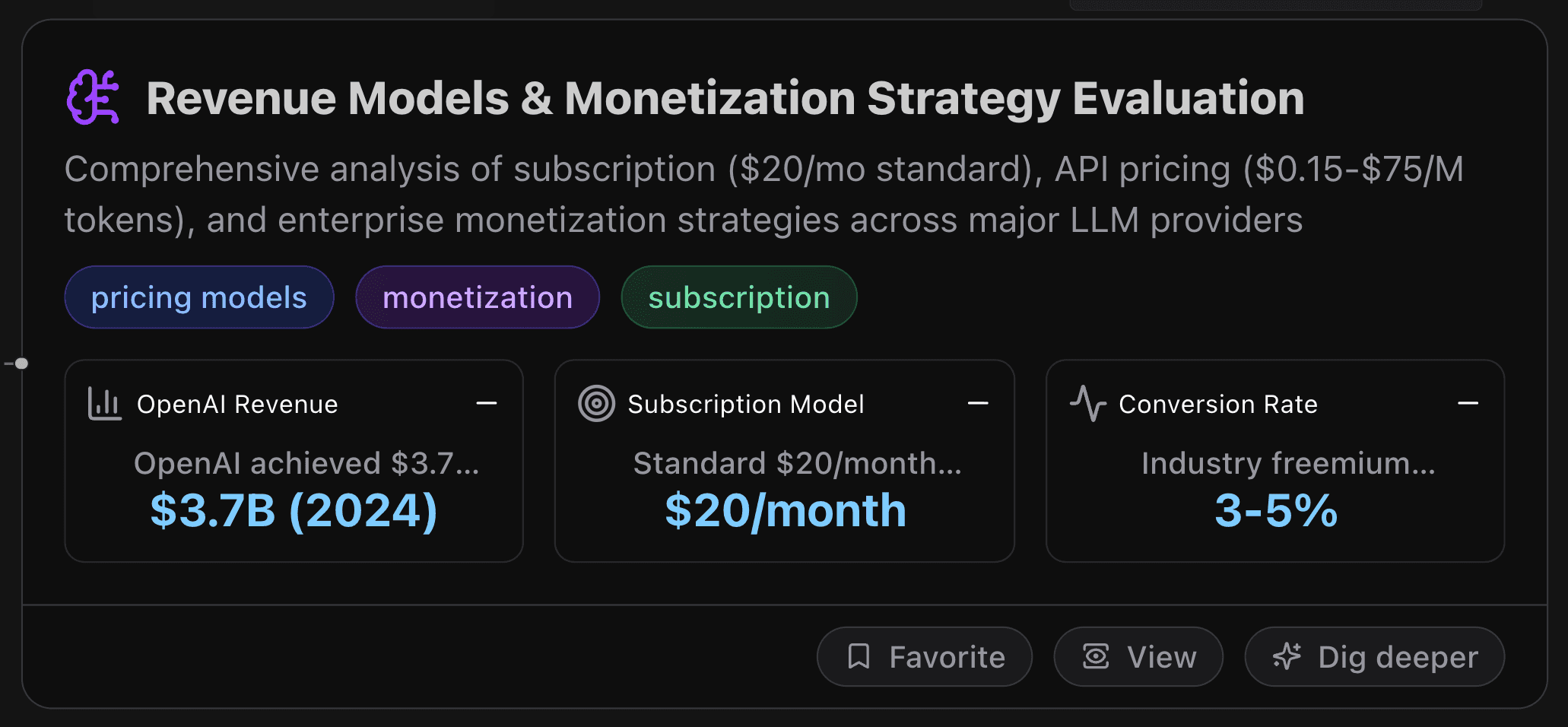

Revenue Models & Monetization Strategy Evaluation

Comprehensive analysis of subscription ($20/mo standard), API pricing ($0.15-$75/M tokens), and enterprise monetization strategies across major LLM providers.

Key Metrics

OpenAI Revenue

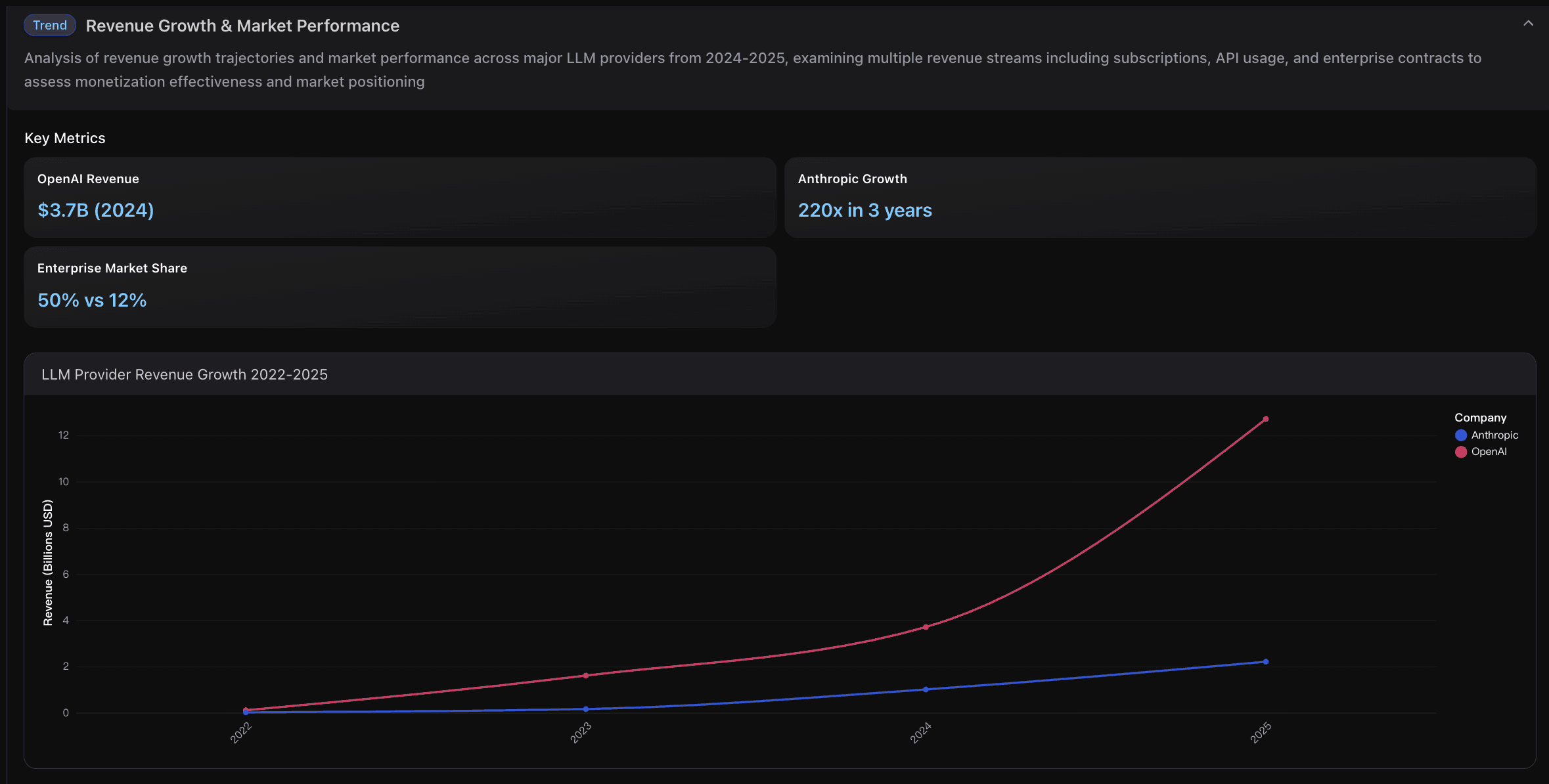

OpenAI achieved $3.7 billion revenue in 2024 with projected $12.7 billion for 2025, representing 243% year-over-year growth. ChatGPT contributed $2.7 billion (75% of total revenue), demonstrating strong consumer monetization through $20/month ChatGPT Plus subscriptions and enterprise contracts.

Subscription Model

Standard $20/month subscription pricing dominates across OpenAI (ChatGPT Plus) and Anthropic (Claude Pro), with ~5% conversion rate from ChatGPT's free users. This freemium-to-premium strategy generated $620 million for Claude Pro subscriptions in H1 2025 alone.

Conversion Rate

Industry freemium conversion rates range 3-5%, with ChatGPT achieving ~5% conversion from 400 million active users to paid subscriptions. Low conversion rates reflect market immaturity but indicate massive monetization potential as willingness-to-pay develops among users.

Actionable Insights

Implement Hybrid Pricing Strategy

Major providers should adopt Anthropic's API-first approach combined with OpenAI's subscription success. Focus on 70-75% API revenue through enterprise contracts while maintaining $20/month consumer subscriptions. This dual-stream approach maximizes both volume (enterprise) and recurring revenue (consumer) while reducing customer acquisition costs.

Optimize Token Pricing Elasticity

Deploy dynamic pricing models that balance the 1000x cost reduction in inference costs with frontier model premiums. Target the $3.50 median enterprise pricing sweet spot while offering ultra-premium tiers at $60-$750 per million tokens for cutting-edge capabilities, capturing both price-sensitive and performance-demanding segments.

Accelerate Enterprise Conversion

Capitalize on the 90% planned AI spending increases by developing enterprise-specific features and dedicated sales teams. Focus on the 50% to 12% market share shift favoring safety-focused models, positioning products around reliability, safety, and compliance to capture enterprise budgets doubling year-over-year.

Data Visualization

Below is a data visualization example:

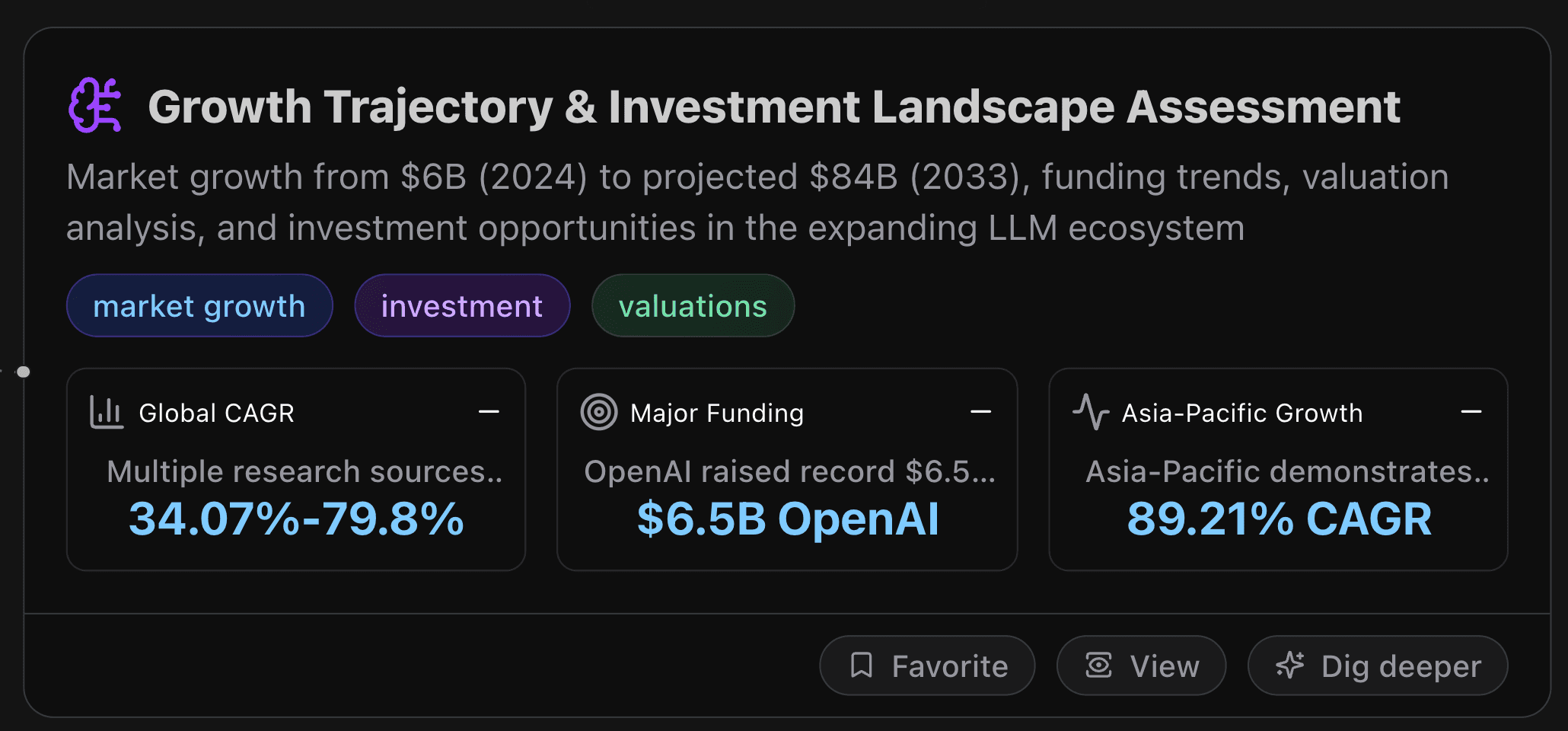

Growth Trajectory & Investment Landscape Assessment

This node analyzes the market growth from $6B (2024) to projected $84B (2033), funding trends, valuation analysis, and investment opportunities in the expanding LLM ecosystem.

Key Metrics

Global CAGR

Multiple research sources project dramatic compound annual growth rates, with conservative estimates at 34.07% (Straits Research) forecasting $84.25B by 2033, while Business Research Insights projects aggressive 79.8% CAGR reaching $1,510B by 2033, indicating significant market expansion potential despite forecast variance.

Major Funding

OpenAI raised record $6.5B funding round demonstrating massive capital requirements for LLM development, while other major players like Anthropic and xAI continue seeking additional funding, indicating sustained investor confidence despite astronomical development costs and competitive pressures.

Asia-Pacific Growth

Asia-Pacific demonstrates highest regional growth rate at 89.21% CAGR, targeting $94B by 2030 from $416M in 2023, driven by China's $30B infrastructure initiatives, India's ₹10,372 crore IndiaAI Mission, and Japan-Korea manufacturing integration, outpacing global average growth significantly.

Actionable Insights

Diversified Investment Strategy

Given the dramatic growth forecasts ranging from 34.07% to 79.8% CAGR and market projections of $84B to $1.5T by 2033, consider a diversified investment approach targeting both established players (OpenAI, Anthropic) and emerging regional leaders, particularly in Asia-Pacific where 89.21% CAGR offers highest growth potential while managing forecast uncertainty through portfolio allocation.

Enterprise Adoption Gap Opportunity

With 92% of Fortune 500 companies using consumer AI tools but only 5% adopting enterprise-grade solutions, focus investment on companies bridging this adoption gap through enterprise-focused LLM platforms, integration services, and compliance-ready solutions, as enterprise spending surge from $3.5B to $8.4B in mid-2025 indicates massive monetization potential.

Geographic Market Positioning

Capitalize on regional expansion by investing in Asia-Pacific market entry strategies targeting $94B opportunity by 2030, particularly China's $10B domestic market and India's government-backed ₹10,372 crore IndiaAI Mission, while leveraging North America's 42% market dominance and Europe's $56M open-source initiatives for balanced geographic exposure and risk mitigation.

Data Visualization

Below is a data visualization example:

User Adoption & Use Cases

If you think the three nodes of the first layer are not exactly the directions you want to know, just click "Ask more", and enter your own question, for example, "User Adoption & Use Cases".

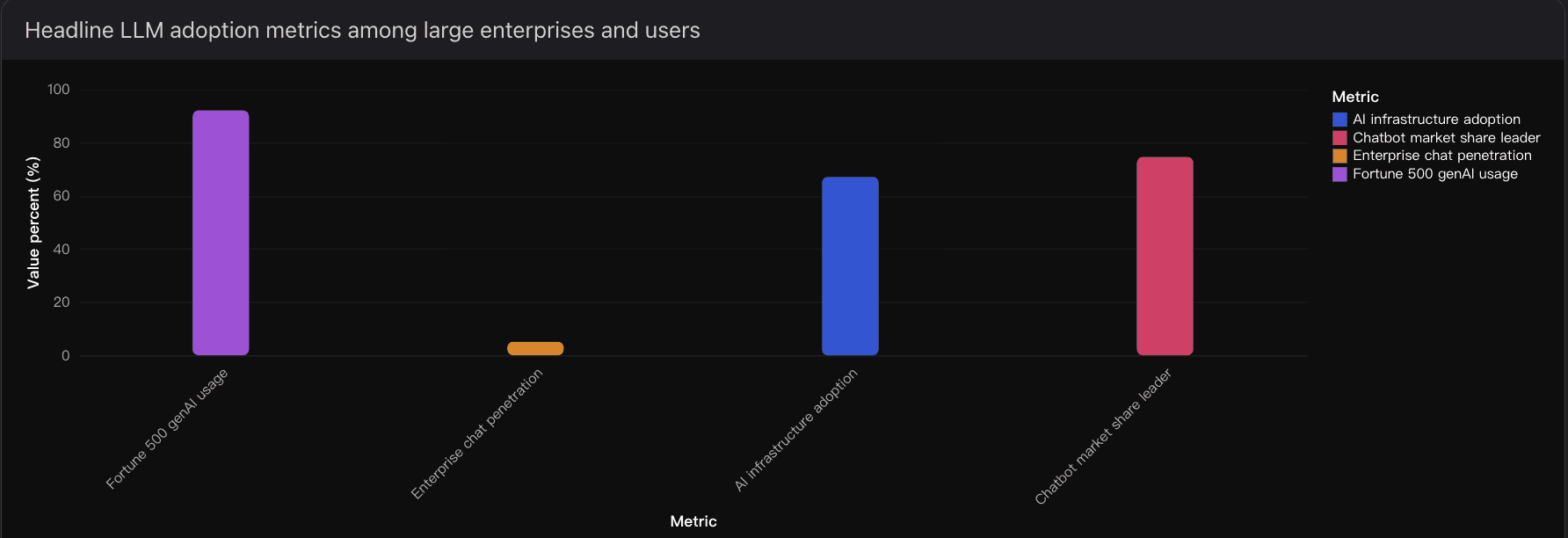

Adoption snapshot and momentum: 1) Enterprise breadth: Approximately 92% of Fortune 500 report using generative AI in workflows, indicating near-ubiquitous exposure and initial integration. 2) Depth of enterprise-grade deployment: Dedicated enterprise chat (e.g., ChatGPT Enterprise and Teams) penetration remains limited at about 5% of the Fortune 500, reflecting ongoing security, compliance, and ROI gating. 3) Infrastructure footprint: Roughly 67% of Fortune 500 have adopted AI infrastructure initiatives, signaling foundational readiness for scaled deployments. 4) Spending acceleration: Enterprise LLM spending rose to about 8.4B USD by mid-2025, up from about 3.5B USD in late 2024, underscoring rapid scale-up toward production. 5) End-user preference: Chatbot market share remains concentrated; ChatGPT’s share has hovered around 74%–75% through 2025, indicating a durable lead in user familiarity and access.

Regional notes that influence adoption: North America continues to lead enterprise rollouts, benefiting from hyperscaler investment and mature governance. APAC is expanding fastest, buoyed by national AI programs and local-language LLMs that unlock new user segments. Europe’s adoption is steady and increasingly shaped by compliance requirements that prioritize model governance, auditability, and data residency.

Where LLMs are delivering sustained value today: 1) Productivity copilots across office suites and CRM/ERP: Writing assistance, meeting summarization, email drafting, and spreadsheet/formula support drive immediate time savings. 2) Customer support automation: Tier-1 deflection, knowledge search, and agent assist lower handle times and improve resolution quality, with safe escalation paths. 3) Developer experience and code generation: Code completion, refactoring, unit tests, migration guides, and secure-by-default scaffolding accelerate delivery and improve consistency. 4) Analytics and decision support: Natural-language BI, SQL generation, and commentary layers shorten time-to-insight; guardrails and verification reduce hallucination risk. 5) Knowledge management and enterprise search: Retrieval-augmented generation over enterprise content improves accuracy and trust, especially with document-level attribution. 6) Content and marketing operations: Multichannel content creation, localization, and A/B variant generation at scale with governed brand voice. 7) Agentic workflows: Structured multi-step automations for routine operations such as ticket triage, quote-to-cash, data cleanup, and back-office tasks, increasingly embedded inside SaaS. 8) Industry-specific patterns: Healthcare scribe and prior-authorization prep, financial research synthesis and KYC enrichment, manufacturing quality logs summarization, and legal clause extraction and review.

Observed adoption patterns and what they imply: 1) Embedded beats standalone: Users adopt faster when LLMs are natively embedded in familiar SaaS (e.g., office suites, CRM, service desks) rather than as net-new tools. 2) Guardrails first: Security, privacy, and provenance controls determine enterprise velocity; solutions with strong data controls and audit trails see faster productionization. 3) ROI clarity: Use cases with measurable KPIs, such as case deflection rates, developer velocity, or time-to-first-draft, scale fastest. 4) Retrieval and verification: RAG with source citations and lightweight output verification (e.g., SQL or policy checks) improves trust and boosts adoption in analytics and support. 5) Agentic shift: Early agent deployments focus on narrow, deterministic tasks with human-in-the-loop; teams expand scope as reliability data accumulates.

Practical guidance for near-term rollout: 1) Prioritize two to three high-ROI workflows: customer support deflection, developer productivity, and sales enablement are reliable first wins. 2) Build the governance spine early: policy templates, data retention rules, audit logging, and approval flows reduce friction later. 3) Instrument outcomes: track deflection rate, mean time saved per user, and quality-of-service metrics tied to business outcomes. 4) Choose models by task, not hype: mix state-of-the-art models for reasoning-heavy tasks with efficient models for high-volume work to balance cost and performance. 5) Plan for change management: adoption improves with enablement content, sandbox environments, and internal champions.

Key numbers to keep in view for decision-making include: Fortune 500 genAI usage at about 92%; enterprise chat penetration around 5%; AI infrastructure adoption near 67%; enterprise LLM spend near 8.4B USD by mid-2025, up from about 3.5B USD in late 2024; and leading chatbot market share at roughly 74%–75%. As shown below, these headline metrics illustrate breadth versus depth in adoption.

What is next: Expect broader rollout of governed copilots within core SaaS suites, incremental expansion of agentic workflows with human oversight, and faster APAC adoption as localized models proliferate. As token prices fall but usage per task rises, cost management will hinge on workload routing and caching, while ROI will increasingly rely on end-to-end workflow redesign rather than isolated prompts.

Conclusion

The global LLM market is entering a defining chapter. OpenAI continues to dominate the consumer landscape with unmatched reach, while Anthropic is rapidly gaining enterprise trust through its safety-first positioning, and Google leverages ecosystem integration to defend its productivity suite stronghold. This competitive triangulation underscores that no single strategy—whether first-mover advantage, technical performance, or ecosystem lock-in—is sufficient on its own. Success will depend on a balanced approach that adapts to shifting user expectations and regulatory realities.

Monetization strategies are also maturing. The combination of consumer subscriptions, enterprise contracts, and API-based models is creating diversified revenue streams, while dynamic token pricing reflects both cost declines and premium demand for frontier capabilities. Yet adoption patterns reveal a crucial gap: although nearly all Fortune 500 companies experiment with generative AI, fewer than 5% have fully deployed enterprise-grade solutions. Bridging this gap will require strong governance, clear ROI, and trust-building through compliance and security.

Growth prospects remain extraordinary, with forecasts ranging from $84 billion to $1.5 trillion by 2033. Asia-Pacific in particular represents the fastest-growing region, propelled by government investment and localized model development. However, scaling this growth will require solving bottlenecks around compute availability, energy efficiency, and responsible AI oversight.

For enterprises, the near-term priority is to identify high-value use cases—such as customer support automation, developer acceleration, and sales enablement—while building a governance backbone that can scale. For investors, diversification across leading incumbents and emerging regional challengers provides the best hedge against forecast uncertainty. And for technology leaders, the shift from standalone LLMs to embedded copilots and agentic workflows signals the direction of future innovation.

Ultimately, the LLM market is not just about bigger models or higher benchmarks—it is about embedding intelligence into the workflows, industries, and societies of tomorrow. Those who combine technical excellence with trust, usability, and ecosystem depth will define the next era of the AI revolution.